Charitable Giving Can Be a Family Affair

As families grow in size and overall wealth, a desire to "give back" often becomes a priority.

Cultivating philanthropic values can help foster responsibility and a sense of purpose among both young and old alike, while providing financial benefits. Charitable donations may be eligible for income tax deductions (if you itemize) and can help reduce capital gains and estate taxes. Here are four ways to incorporate charitable giving into your family's overall financial plan.

Annual Family Giving

The holidays present a perfect opportunity to help family members develop a giving mindset. To establish an annual family giving plan, first determine the total amount that you'd like to donate as a family to charity. Next, encourage all family members to research and make a case for their favorite nonprofit organization, or divide the total amount equally among your family members and have each person donate to his or her favorite cause.

When choosing a charity, consider how efficiently the contribution dollars are used — i.e., how much of the organization's total annual budget directly supports programs and services versus overhead, administration, and marketing. For help in evaluating charities, visit the Charity Navigator web site, charitynavigator.org, where you'll find star ratings and more detailed financial and operational information.

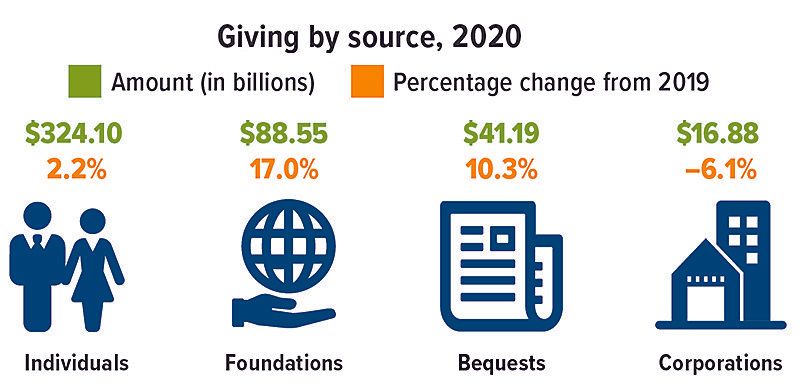

Snapshot of 2020 Giving

Despite the pandemic and economic downturn, 2020 was the highest year for charitable giving on record, reaching $471.44 billion. Giving to public-society benefit organizations, environmental and animal organizations, and human services organizations grew the most, while giving to arts, culture, and humanities and to health organizations declined.

Estate Planning

Charitable giving can also play a key role in an estate plan by helping to ensure that your philanthropic wishes are carried out and potentially reducing your estate tax burden.

The federal government taxes wealth transfers both during your lifetime and at death. In 2021, the federal gift and estate tax is imposed on lifetime transfers exceeding $11,700,000, at a top rate of 40%. States may also impose taxes but at much lower thresholds than the federal government.

Ways to incorporate charitable giving into your estate plan include will and trust bequests; beneficiary designations for insurance policies and retirement plan accounts; and charitable lead and charitable remainder trusts. (Trusts incur upfront costs and often have ongoing administrative fees. The use of trusts involves complex tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax professionals before implementing such strategies.)

Donor-Advised Funds

Donor-advised funds offer a way to receive tax benefits now and make charitable gifts later. A donor-advised fund is an agreement between a donor and a host organization (the fund). Your contributions are generally tax deductible, but the organization becomes the legal owner of the assets. You (or a designee, such as a family member) then advise on how those contributions will be invested and how grants will be distributed. (Although the fund has ultimate control over the assets, the donor's wishes are generally honored.)

Family Foundations

Private family foundations are similar to donor-advised funds, but on a more complex scale. Although you don't necessarily need the coffers of Melinda Gates or Sam Walton to establish and maintain one, a private family foundation may be most appropriate if you have a significant level of wealth. The primary benefit (in addition to potential tax savings) is that you and your family have complete discretion over how the money is invested and which charities will receive grants. A drawback is that these separate legal entities are subject to stringent regulations.

These are just a few of the ways families can nurture a philanthropic legacy while benefitting their financial situation. For more information, contact your financial professional or an estate planning attorney.

Bear in mind that not all charitable organizations are able to use all possible gifts, so it is prudent to check first. The type of organization you select can also affect the tax benefits you receive.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.