How Much Life Insurance Do You Need?

Throughout your life, your financial needs will change and life insurance can help you meet some of those needs.

But how much life insurance do you need? There are a number of approaches to help determine how much life insurance you should have. Here are three of those methods.

Family Needs Approach

With this approach, you divide your family's financial needs into three main categories:

- Immediate needs at death, such as cash needed for estate taxes and settlement costs, credit-card and other debts including a mortgage (unless you choose to include mortgage payments as part of ongoing family expenses), and an emergency fund for unexpected costs

- Ongoing income needs for expenses such as food, clothing, shelter, and transportation, which will vary in amount and duration, depending on a number of factors, such as your spouse's age, your children's ages, your surviving spouse's income, your debt, and whether you'll provide funds for your surviving spouse's retirement

- Special funding needs, such as college, charitable bequests, funding a buy/sell agreement, or business succession planning

Once you determine the total amount of your family's financial needs, subtract that total from the available assets your family could use to help defray some or all of these expenses. The difference, if any, represents an amount that the life insurance proceeds, and the income from future investment of those proceeds, might cover.

Income Replacement Calculation

This method is based on the premise that family income earners should buy enough life insurance to replace the loss of income due to an untimely death. Under this approach, the amount of life insurance you should consider is based on the value of the income that you can expect to earn during your lifetime, taking into account such factors as inflation and anticipated salary increases, as well as the interest that the lump-sum life insurance proceeds may generate.

Estate Preservation and Liquidity Needs Approach

This method attempts to calculate the amount of life insurance needed to settle your estate. Settlement costs may include estate taxes and funeral, legal, and accounting expenses. The goal is to preserve the value of your estate at the level prior to your death and to avoid an unwanted sale of assets to pay for any of these estate settlement expenses. This approach takes into consideration the amount of life insurance you may want in order to maintain the current value of your estate for your family, while providing the cash needed to cover death expenses and taxes.

Unfortunately, many people underestimate their life insurance needs. Often, the purchase of life insurance is based solely on its cost instead of the benefit it might provide. By the same token, it's possible to have more life insurance than you need. September is Life Insurance Awareness Month, a good time to review your life insurance to help ensure that it matches your current and projected needs.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. Any guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company. Optional benefits are available for an additional cost and are subject to contractual terms, conditions, and limitations.

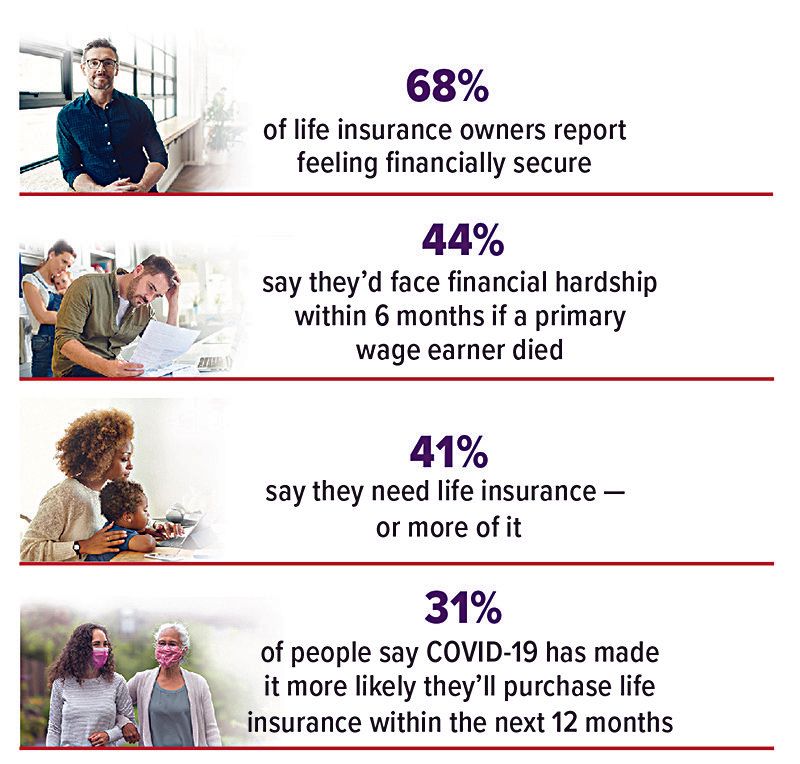

Interest in Life Insurance Stays Strong

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.