When Two Goals Collide: Balancing College and Retirement Preparations

You've been doing the right thing financially for many years, saving for your child's education and your own retirement. Yet now, as both goals loom in the years ahead, you may wonder what else you can do to help your child (or children) receive a quality education without compromising your own retirement goals.

Knowledge Is Power

Start by reviewing the financial aid process and understanding how financial need is calculated. Colleges and the federal government use different formulas to determine need by looking at a family's income (the most important factor), assets, and other household information.

A few key points:

- Generally, the federal government assesses up to 47% of parent income (adjusted gross income plus untaxed income/benefits minus certain deductions) and 50% of a student's income over a certain amount. Parent assets are counted at 5.6%; student assets are counted at 20%.(1)

- Certain parent assets are excluded, including home equity and retirement assets.

- The Free Application for Federal Student Aid (FAFSA) relies on your income from two years prior (the "base year") and current assets for its analysis. For example, for the 2023-2024 school year, the FAFSA will consider your 2021 income tax record and your assets at the time of application.

Strategies to Consider

Financial aid takes two forms: need-based aid and merit-based aid. Although middle- and higher-income families typically have a tougher time receiving need-based aid, there are some ways to reposition your finances to potentially enhance eligibility:

- Time the receipt of discretionary income to avoid the base year.

- Have your child limit his or her income during the base year to the excludable amount.

- Use countable assets (such as cash savings) to increase investments in your college and retirement savings accounts and pay down consumer debt and your mortgage.

- Make a major purchase, such as a car or home improvement, to reduce liquid assets.

Many colleges use merit-aid packages to attract students, regardless of financial need. As your family explores colleges in the years ahead, be sure to investigate merit-aid opportunities as well. A net price calculator, available on every college website, can give you an estimate of how much financial aid (merit- and need-based) your child might receive at a particular college.

Don't Lose Sight of Retirement

What if you've done all you can and still face a sizable gap between how much college will cost and how much you have saved? To help your child graduate with as little debt as possible, you might consider borrowing or withdrawing funds from your retirement savings. Though tempting, this is not an ideal move. While your child can borrow to finance his or her education, you generally cannot take a loan to fund your retirement. If you make retirement savings and debt reduction (including a mortgage) a priority now, you may be better positioned to help your child repay any loans later.

Consider speaking with a financial professional about how these strategies may help you balance these two challenging and important goals. There is no assurance that working with a financial professional will improve investment results.

Withdrawals from traditional IRAs and most employer-sponsored retirement plans are taxed as ordinary income and may be subject to a 10% penalty tax if taken prior to age 59½, unless an exception applies. (IRA withdrawals used for qualified higher-education purposes avoid the early-withdrawal penalty.)

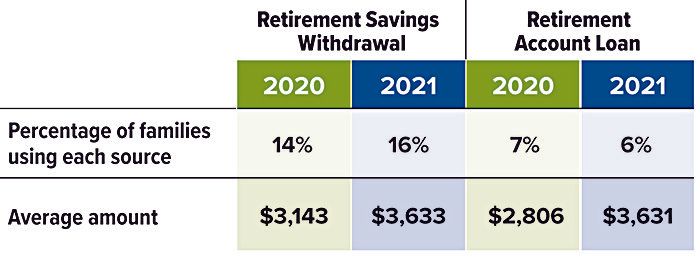

Some Parents Use Retirement Funds to Pay for College

(1) College Savings Plan Network, 2021

All Securities Through Money Concepts Capital Corp., Member FINRA / SIPC

11440 North Jog Road, Palm Beach Gardens, FL 33418 Phone: 561.472.2000

Copyright 2010 Money Concepts International Inc.

Investments are not FDIC or NCUA Insured

May Lose Value - No Bank or Credit Union Guarantee

This communication is strictly intended for individuals residing in the state(s) of MI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2020.